Autor: Jarosław Jamka

My key takeaways:

1) First, it’s going to be flat nominal growth at best. And this in an environment of high inflation. Investors should probably get used to this. The company is too large for any new and innovative products to significantly accelerate the growth of total revenues (in the short term).

2) If investors „accept flat growth” – then practically all other important factors related to the company are fine and solid – starting from a strong brand, customer satisfaction, market position, margins, further products, Vision Pro, expectations regarding AI applications, growing dividend and increasingly larger share buybacks, etc.

Tim Cook, CEO:

„In services, we set an all-time revenue record, up 14% over the past year. Keep in mind, as we described on the last call, in the March quarter a year-ago, we were able to replenish iPhone channel inventory and fulfill significant pent-up demand from the December quarter COVID-related supply disruptions on the iPhone 14 Pro and 14 Pro Max. We estimate this one-time impact added close to $5 billion to the March quarter revenue last year. If we remove this from last year’s results, our March quarter total company revenue this year would have grown.”

And about GenAI:

„We continue to feel very bullish about our opportunity in Generative AI. We are making significant investments, and we’re looking forward to sharing some very exciting things with our customers soon. We believe in the transformative power and promise of AI, and we believe we have advantages that will differentiate us in this new era, including Apple’s unique combination of seamless hardware, software and services integration, groundbreaking Apple’s silicon, with our industry-leading neural engines and our unwavering focus on privacy”

And the remaining takeaways:

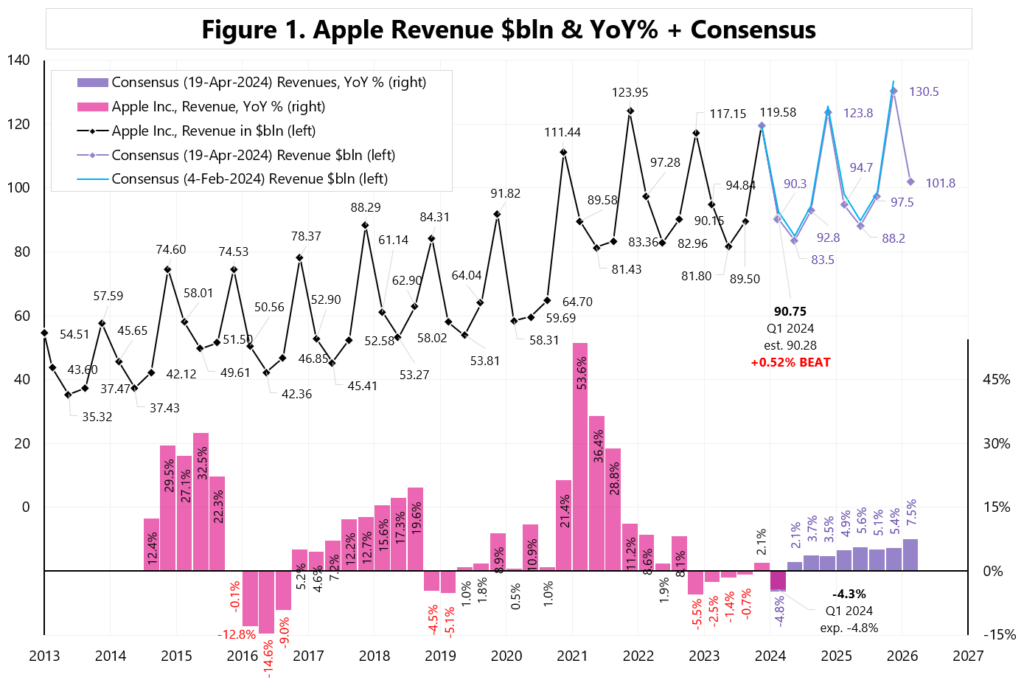

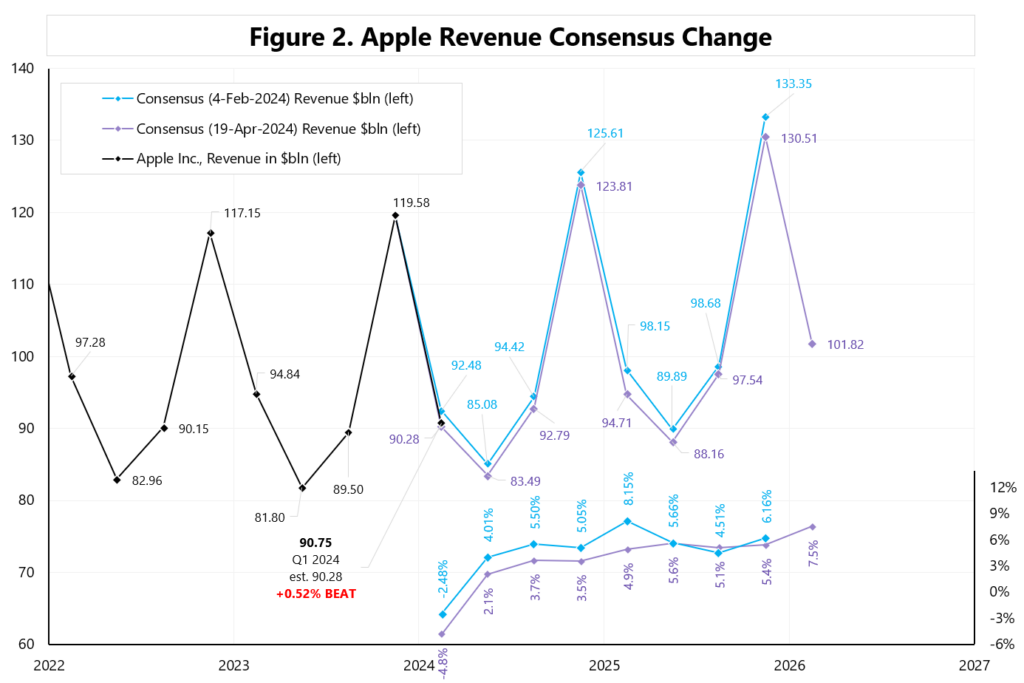

3) Revenues decreased YoY by 4.8% and this is the 5th quarter of negative annual growth over the last 6 quarters – see Figure 1. A year ago, approximately $5 billion in iPhone sales moved from Q4 2022 to Q1 2023 – if we adjusted the results for this, then Q4 would be negative (-2.1%) and the current quarter positive (+1.02%). It is also worth noting the significant decline in Wall Street expectations regarding Apple’s revenue growth – see Figure 2 (and comparison of the consensus change from February to April 2024).

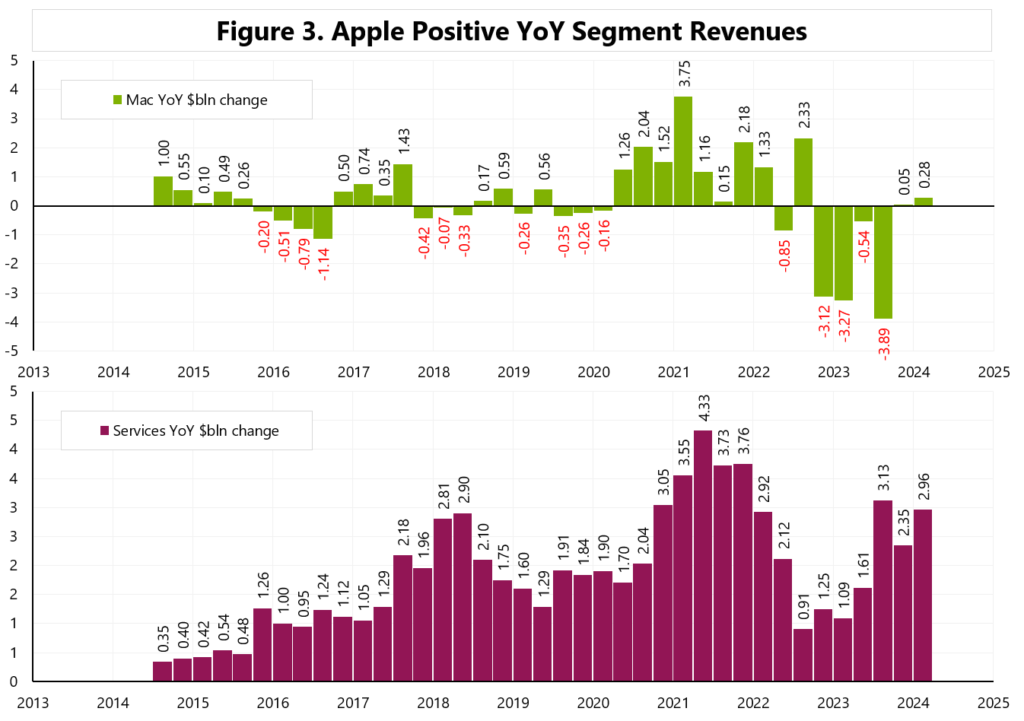

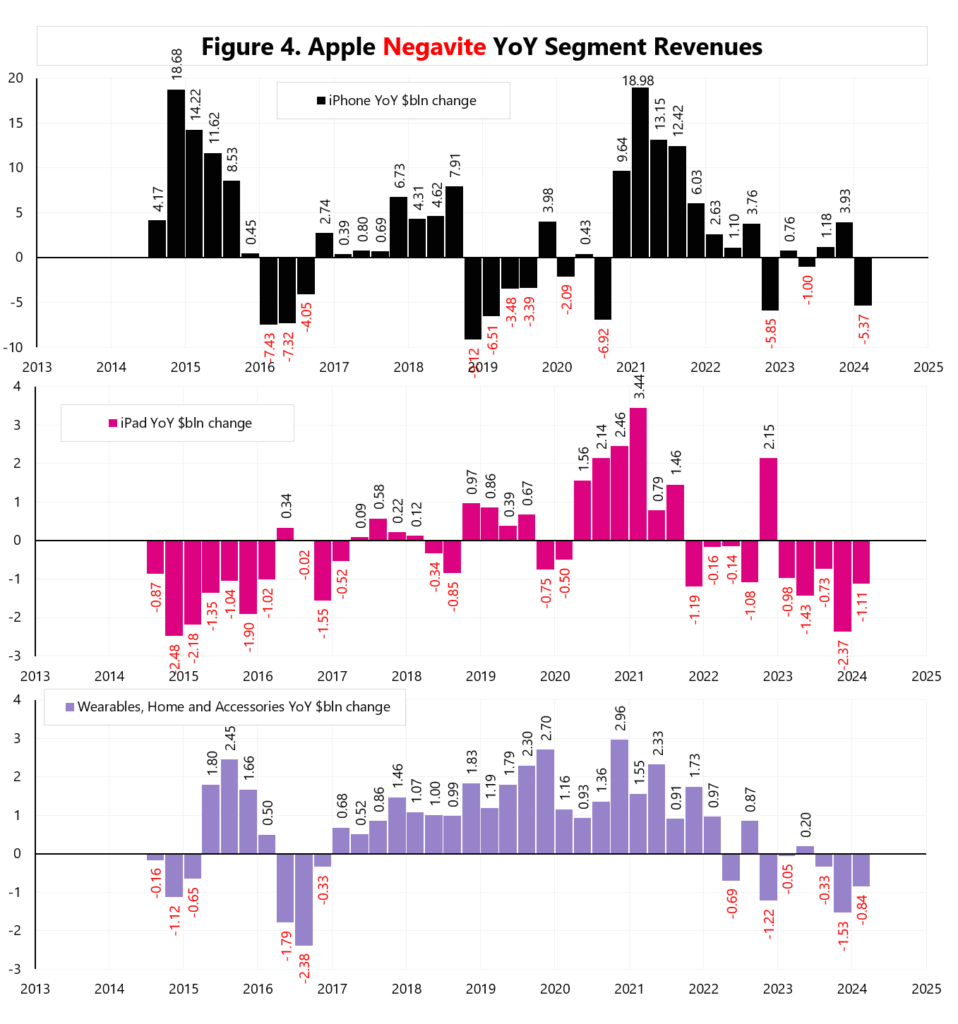

4) Year over year, Apple recorded revenue growth only on Mac sales (+$0.28 billion YoY) and Services (+$2.96 billion) – see Figure 3. The remaining product categories were negative year over year – see Figure 4.

5) To counterbalance and somehow satisfy shareholders… Apple increased its share buyback program to $110 billion and also increased its dividend by 4% to $0.25 per share.

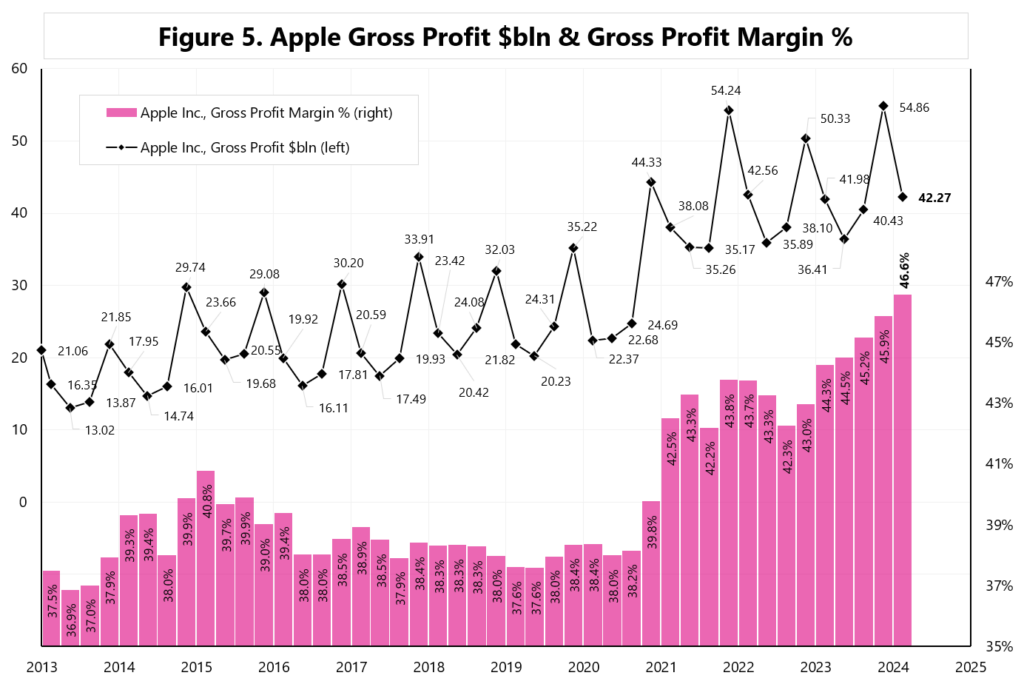

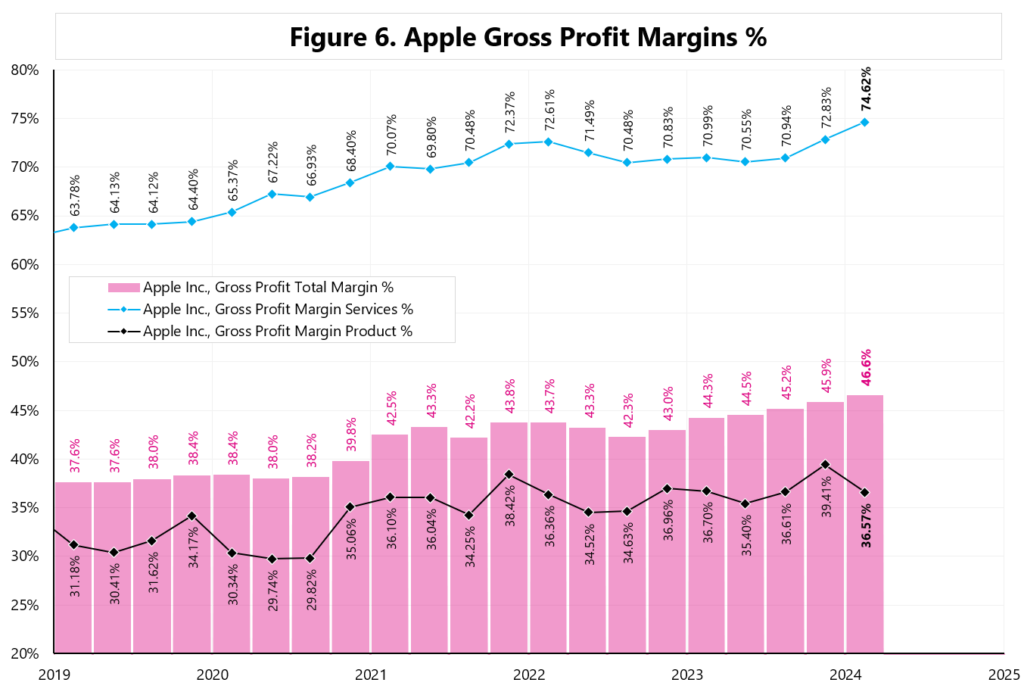

6) Revenues may not be growing as investors would like, but in return the gross profit margin is constantly growing – and in Q1 it reached as much as 46.6% – see Figure 5. This is due to growing margins in services (and falling margins on products) – see Figure 6.

Luca Maestri, CFO:

„Company gross margin was 46.6%, up 70 basis points sequentially, driven by cost savings and favorable mix to services, partially offset by leverage. Products gross margin was 36.6%, down 280 basis points sequentially, primarily driven by seasonal loss of leverage and mix, partially offset by favorable costs. Services gross margin was 74.6%, up 180 basis points from last quarter due to a more favorable mix.”

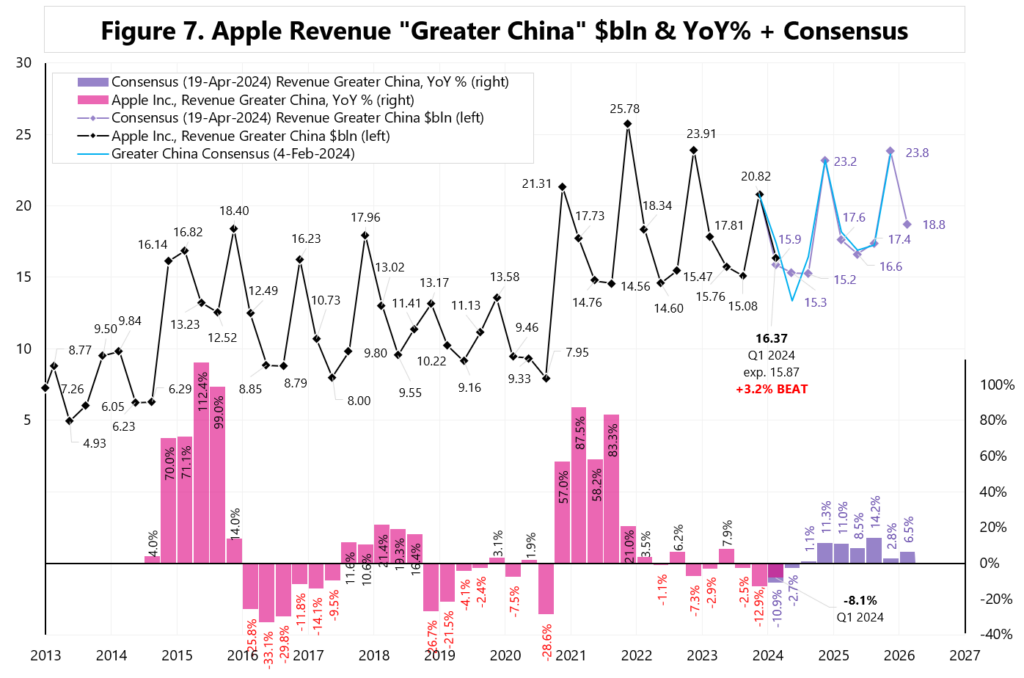

7) Investors pay a lot of attention to the Chinese market (there were a lot of questions about China at the results conference). Sales in the Chinese market decreased YoY by 8.1% (-$1.44 billion). This is a smaller decline than in the previous quarter, when it amounted to -12.9%. See Figure 7. However, the company remains optimistic about the Chinese market…

Tim Cook:

„(…) if you look at our results in Q2 for Greater China, we were down 8%. That’s an acceleration from the previous quarter in Q1. And the primary driver of the acceleration was iPhone. And if you then look at iPhone within Mainland China, we grew on a reported basis. That’s before any kind of normalization for the supply disruption that we mentioned earlier. And if you look at the top-selling smartphones, the Top 2 in Urban China are iPhones. And while I was there, it was a great visit and we opened a new store in Shanghai and the reception was very warm and highly energetic (…). And so I maintain a great view of China in the long-term. I don’t know how each and every quarter goes and each and every week. But over the long haul, I have a very positive viewpoint.”

Niniejszy materiał jest informacją reklamową. Ma charakter edukacyjno-informacyjny i stanowi wyraz własnych ocen, przemyśleń i opinii autora. Niniejszy materiał służy jedynie celom informacyjnym i nie stanowi oferty, w tym oferty w rozumieniu art. 66 oraz zaproszenia do zawarcia umowy w rozumieniu art. 71 ustawy z dnia 23 kwietnia 1964 r. – Kodeks cywilny (t.j. Dz. U. z 2020 r. poz. 1740, 2320), ani oferty publicznej w rozumieniu art. 3 ustawy z dnia 29 lipca 2005 r. o ofercie publicznej i warunkach wprowadzania instrumentów finansowych do zorganizowanego systemu obrotu oraz o spółkach publicznych (t.j. Dz. U. z 2022 r. poz. 2554, z 2023 r. poz. 825, 1723) czy też oferty publicznej w rozumieniu art 2 lit d) Rozporządzenia Parlamentu Europejskiego i Rady (UE) 2017/1129 z dnia 14 czerwca 2017 r. w sprawie prospektu, który ma być publikowany w związku z ofertą publiczną papierów wartościowych lub dopuszczeniem ich do obrotu na rynku regulowanym oraz uchylenia dyrektywy 2003/71/WE (Dz. Urz. UE L 168 z 30.06.2017, str. 12); Niniejszy materiał nie stanowi także rekomendacji, zaproszenia, ani usług doradztwa. prawnego, podatkowego, finansowego lub inwestycyjnego, związanego z inwestowaniem w jakiekolwiek papiery wartościowe. Materiał ten nie może stanowić podstawy do podjęcia decyzji o dokonaniu jakiejkolwiek inwestycji w papiery wartościowe czy instrumenty finansowe. Informacje zamieszczone w materiale nie stanowią rekomendacji w rozumieniu przepisów Rozporządzenia Parlamentu Europejskiego i Rady (UE) NR 596/2014 z dnia 16 kwietnia 2014 r. w sprawie nadużyć na rynku (rozporządzenie w sprawie nadużyć na rynku) oraz uchylające dyrektywę 2003/6/ WE Parlamentu Europejskiego i Rady i dyrektywy Komisji 2003/124/WE, 2003/125/WE i 2004/72/ WE. (Dz. U UE L 173/1 z dnia 12.06.20114). NDM S.A., nie ponosi odpowiedzialności za prawdziwość, rzetelność i kompletność oraz aktualność danych i informacji zamieszczonych w niniejszej prezentacji. NDM S.A. nie ponosi również jakiejkolwiek odpowiedzialności za szkody wynikające z wykorzystania niniejszego materiału, informacji i danych w nim zawartych. Zawartość materiału została przygotowana na podstawie opracowań sporządzonych zgodnie z najlepszą wiedzą NDM S.A. oraz przy wykorzystaniu informacji i danych publicznie dostępnych, chyba, że wyraźnie wskazano inne źródło pochodzenia danych.