Autor: Jarosław Jamka

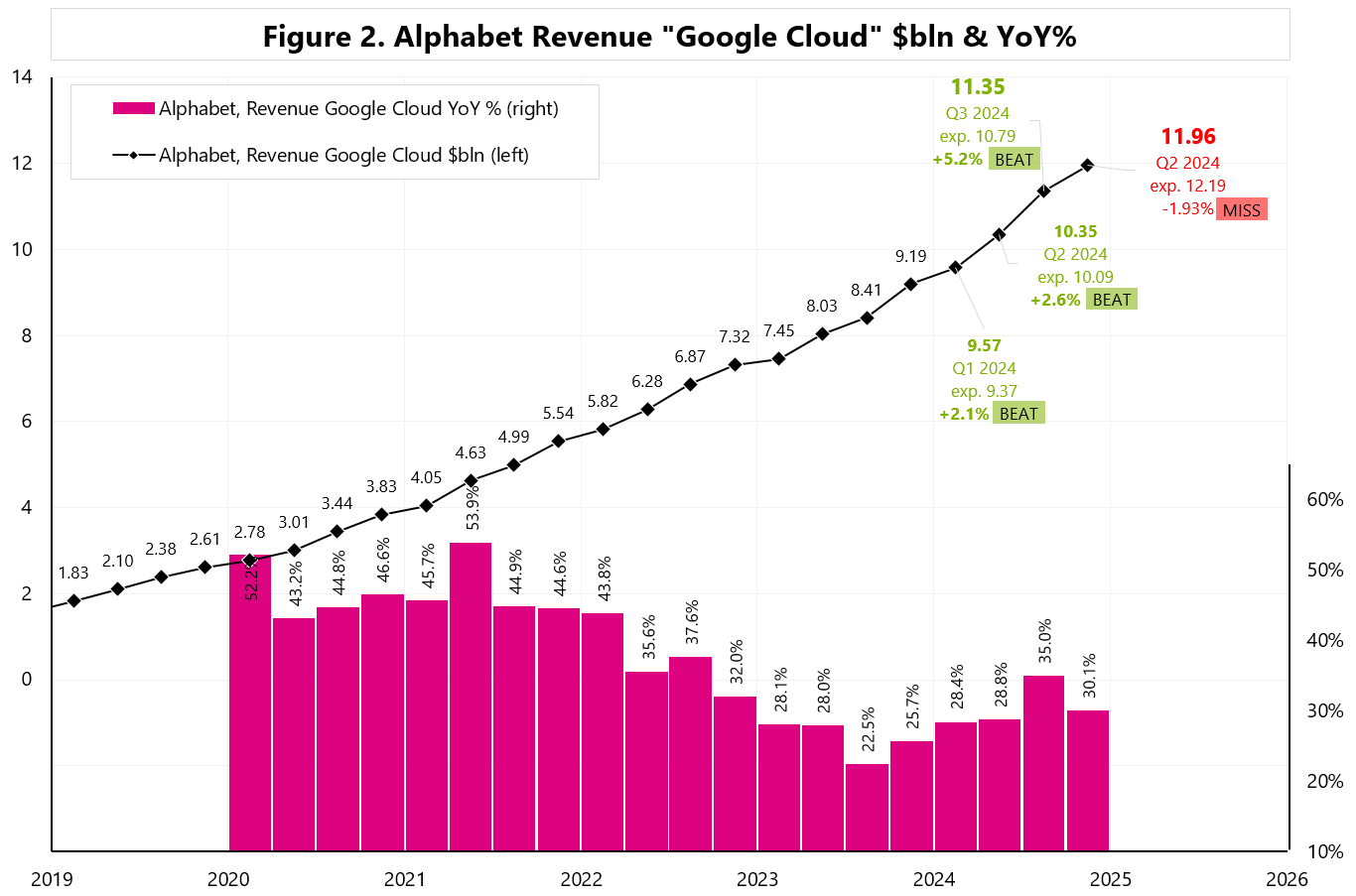

Alphabet generally showed solid results in Q4, but slightly below expectations for total revenue (0.16% miss) – see Figure 1. But the most important thing was the miss on Google Cloud (a whopping 1.93%) – see Figure 2.

The main reason for lower revenue was supply constraints, which prevented Alphabet from meeting the high demand related to AI (negative in the short term, however positive in the long term).

Anat Ashkenazi, CFO:

“On the Cloud question, first, I’m excited that we ended the quarter at $12 billion and a 30% year-over-year growth. Very impressive growth. And as I’ve mentioned in the prepared remarks, GCP grew at a much higher rate than overall Cloud. Two items to think about from a deceleration perspective, the first is we are lapping a very strong quarter [in] AI deployments in Q4 2023. The second is the one you’ve alluded to. We do see and have been seeing very strong demand for our AI products in the fourth quarter of 2024. And we exited the year with more demand than we had available capacity.

So we are in a tight supply-demand situation, working very hard to bring more capacity online. As I mentioned, we’ve increased investment in CapEx in 2024, continuing to increase in 2025. And we’ll bring more capacity throughout the year”.

Alphabet spent $14 billion on CapEx in Q4 2024, but Capex will increase significantly in 2025.

Anat Ashkenazi, CFO:

“Ss we expand our AI efforts, we expect to increase our investments in capital expenditure for technical infrastructure, primarily for servers, followed by data centers and networking.

We expect to invest approximately $75 billion in CapEx in 2025, with approximately $16 billion to $18 billion of that in the first quarter.”

Finally, Sundar Pichai, CEO, commented on DeepSeek:

“A couple of things I would say are, if you look at the trajectory over the past three years, the proportion of the spend towards inference compared to training has been increasing, which is good, because obviously inference is to support businesses with good ROIC. And so I think that trend is good.

I think the reasoning models, if anything, accelerates that trend, because it’s obviously scaling upon inference dimension as well.

And so, look, I think part of the reason we are so excited about the AI opportunity is we know we can drive extraordinary use cases, because the cost of actually using it is going to keep coming down, which will make more use cases feasible, and that’s the opportunity space. It’s as big as it comes, and that’s why you’re seeing us invest to meet that moment.”

Niniejszy materiał jest informacją reklamową. Ma charakter edukacyjno-informacyjny i stanowi wyraz własnych ocen, przemyśleń i opinii autora. Niniejszy materiał służy jedynie celom informacyjnym i nie stanowi oferty, w tym oferty w rozumieniu art. 66 oraz zaproszenia do zawarcia umowy w rozumieniu art. 71 ustawy z dnia 23 kwietnia 1964 r. – Kodeks cywilny (t.j. Dz. U. z 2020 r. poz. 1740, 2320), ani oferty publicznej w rozumieniu art. 3 ustawy z dnia 29 lipca 2005 r. o ofercie publicznej i warunkach wprowadzania instrumentów finansowych do zorganizowanego systemu obrotu oraz o spółkach publicznych (t.j. Dz. U. z 2022 r. poz. 2554, z 2023 r. poz. 825, 1723) czy też oferty publicznej w rozumieniu art 2 lit d) Rozporządzenia Parlamentu Europejskiego i Rady (UE) 2017/1129 z dnia 14 czerwca 2017 r. w sprawie prospektu, który ma być publikowany w związku z ofertą publiczną papierów wartościowych lub dopuszczeniem ich do obrotu na rynku regulowanym oraz uchylenia dyrektywy 2003/71/WE (Dz. Urz. UE L 168 z 30.06.2017, str. 12); Niniejszy materiał nie stanowi także rekomendacji, zaproszenia, ani usług doradztwa. prawnego, podatkowego, finansowego lub inwestycyjnego, związanego z inwestowaniem w jakiekolwiek papiery wartościowe. Materiał ten nie może stanowić podstawy do podjęcia decyzji o dokonaniu jakiejkolwiek inwestycji w papiery wartościowe czy instrumenty finansowe. Informacje zamieszczone w materiale nie stanowią rekomendacji w rozumieniu przepisów Rozporządzenia Parlamentu Europejskiego i Rady (UE) NR 596/2014 z dnia 16 kwietnia 2014 r. w sprawie nadużyć na rynku (rozporządzenie w sprawie nadużyć na rynku) oraz uchylające dyrektywę 2003/6/ WE Parlamentu Europejskiego i Rady i dyrektywy Komisji 2003/124/WE, 2003/125/WE i 2004/72/ WE. (Dz. U UE L 173/1 z dnia 12.06.20114). NDM S.A., nie ponosi odpowiedzialności za prawdziwość, rzetelność i kompletność oraz aktualność danych i informacji zamieszczonych w niniejszej prezentacji. NDM S.A. nie ponosi również jakiejkolwiek odpowiedzialności za szkody wynikające z wykorzystania niniejszego materiału, informacji i danych w nim zawartych. Zawartość materiału została przygotowana na podstawie opracowań sporządzonych zgodnie z najlepszą wiedzą NDM S.A. oraz przy wykorzystaniu informacji i danych publicznie dostępnych, chyba, że wyraźnie wskazano inne źródło pochodzenia danych.