Autor: Jarosław Jamka

My key takeaways:

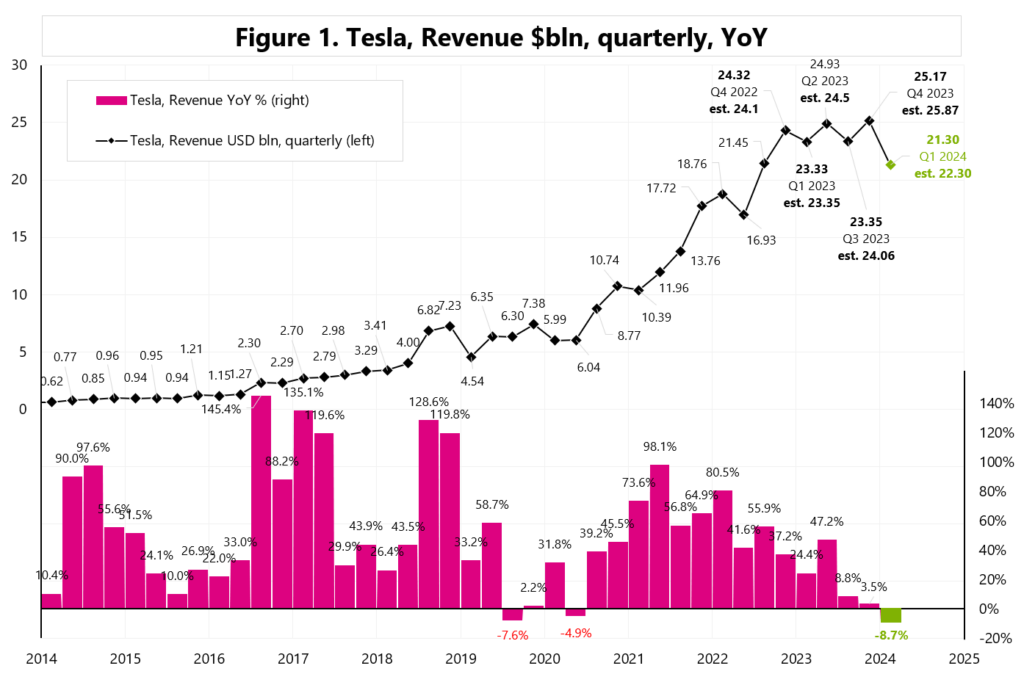

1) Q1 2024 was a terrible quarter, with revenues down 15.4% QoQ and 8.7% YoY. Mainly due to a drop in ASP (vehicle average selling price), but partly due to one-off events (like Giga Berlin production disruptions).

Tesla showed negative free cash flow in Q1, mainly due to higher car production and lower deliveries, but also higher CAPEX. Q2 2024 should be much better.

2) To improve the situation, Tesla cut employment by 10% (The savings generated are expected to be well in excess of $1 billion on an annual run rate basis), and accelerates the introduction of a new cheap car model. It seems that the faster introduction of the new cheap model „saved” the company’s share price. At least for a while.

Elon Musk during earnings call:

“We’ve updated our future vehicle lineup to accelerate the launch of new models ahead, previously mentioned start of production in the second half of 2025. So, we expect it to be more like the early 2025, if not late this year.”

3) Great emphasis during the earnings call is placed on the future fully autonomous version of FSD (full self-driving). This will „unlock” the true value of the company. But we don’t know how long it will take. This could still be years away. Some analysts talk about the 2030s.

But Tesla is well on its way to achieving this, and the latest FSD Version 12 is fully AI-based.

Elon Musk:

“I think Cathie Wood said it best. Like really, we should be thought of as an AI or robotics company. If you value Tesla as just like an auto company, you just have to — fundamentally, it’s just the wrong framework (…). So, I mean, if somebody doesn’t believe Tesla is going to solve autonomy, I think they should not be an investor in the company.”

“(…) the way to think of Tesla is almost entirely in terms of solving autonomy and being able to turn on that autonomy for a gigantic fleet. And I think it might be the biggest asset value appreciation history when that day happens when you can do unsupervised full self-driving.”

4) All in all, is all the worst already priced in the price? Doubtful, car demand will not rebound significantly until interest rates fall. But at least Tesla’s post-earnings rebound of some 12% gives some hope. Yet the real test will be to defend the stock price level before the results were announced, i.e. USD 140-145 range.

Figure 1 shows the revenues $bln and YoY%.

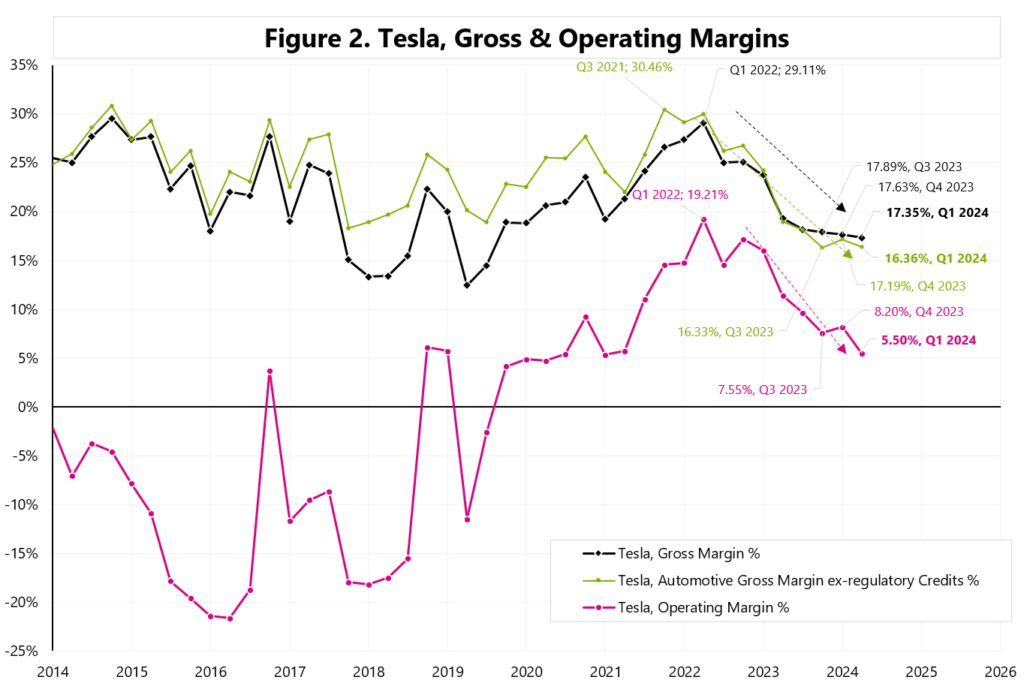

Figure 2 shows Tesla’s margins.

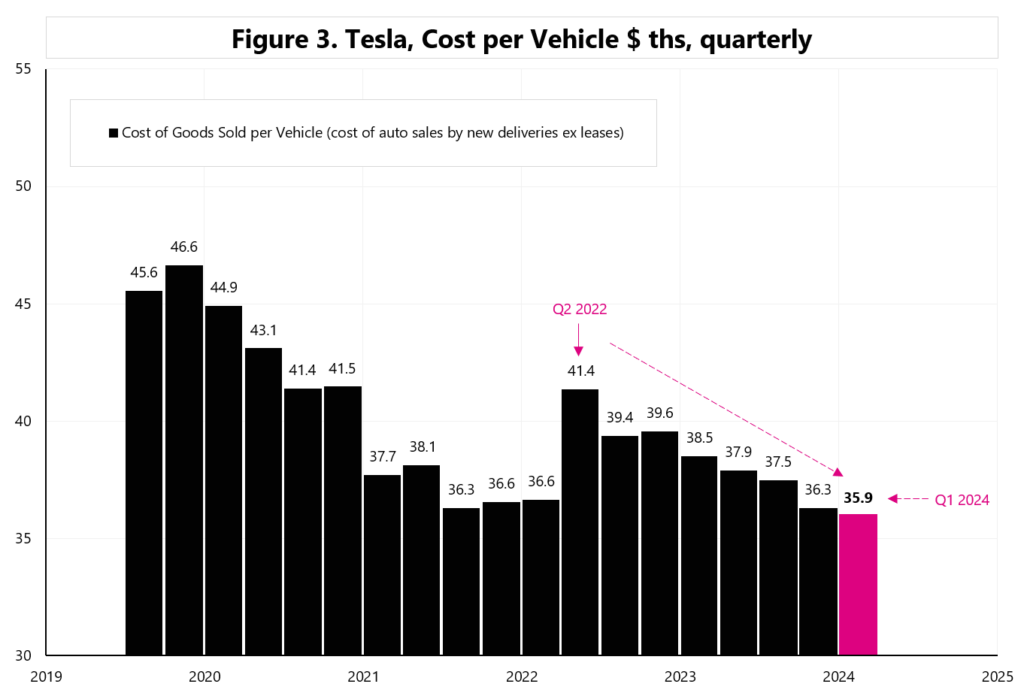

Figure 3 shows Tesla’s avergae cost of vehicle.

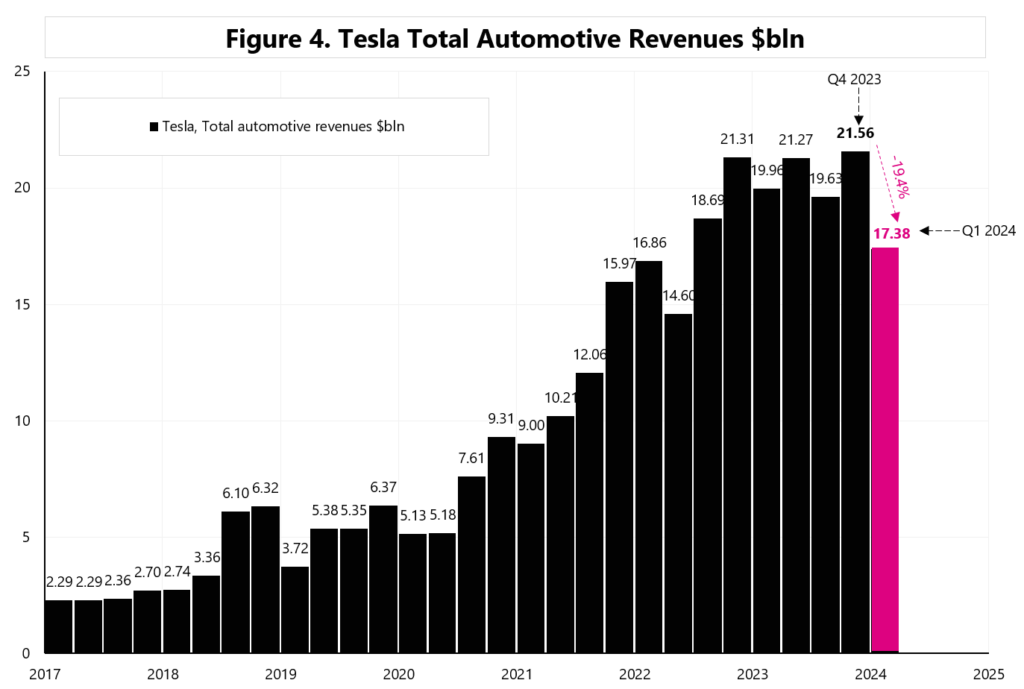

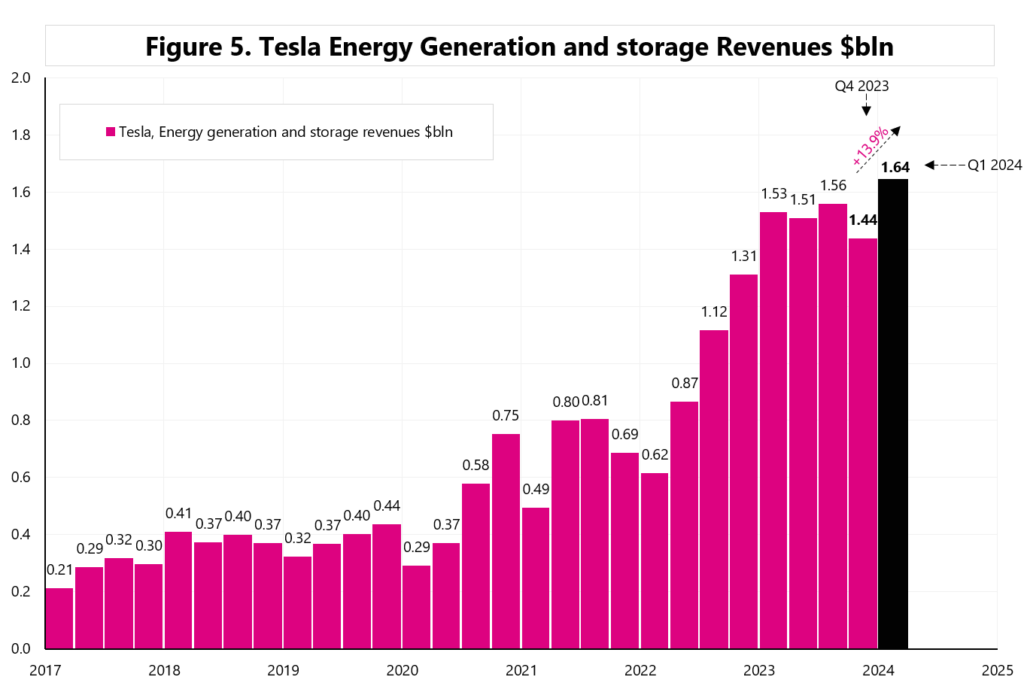

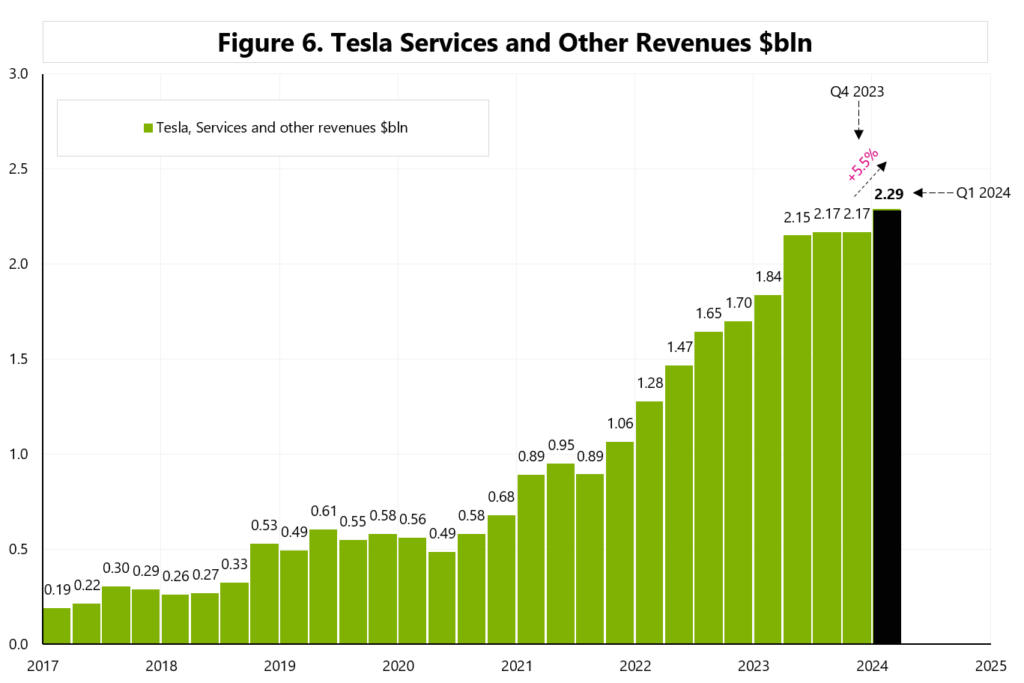

Figure 4-6 show Tesla’s revenue segments (Automotive, Energy Generation & Storage, Services & Other).

Niniejszy materiał jest informacją reklamową. Ma charakter edukacyjno-informacyjny i stanowi wyraz własnych ocen, przemyśleń i opinii autora. Niniejszy materiał służy jedynie celom informacyjnym i nie stanowi oferty, w tym oferty w rozumieniu art. 66 oraz zaproszenia do zawarcia umowy w rozumieniu art. 71 ustawy z dnia 23 kwietnia 1964 r. – Kodeks cywilny (t.j. Dz. U. z 2020 r. poz. 1740, 2320), ani oferty publicznej w rozumieniu art. 3 ustawy z dnia 29 lipca 2005 r. o ofercie publicznej i warunkach wprowadzania instrumentów finansowych do zorganizowanego systemu obrotu oraz o spółkach publicznych (t.j. Dz. U. z 2022 r. poz. 2554, z 2023 r. poz. 825, 1723) czy też oferty publicznej w rozumieniu art 2 lit d) Rozporządzenia Parlamentu Europejskiego i Rady (UE) 2017/1129 z dnia 14 czerwca 2017 r. w sprawie prospektu, który ma być publikowany w związku z ofertą publiczną papierów wartościowych lub dopuszczeniem ich do obrotu na rynku regulowanym oraz uchylenia dyrektywy 2003/71/WE (Dz. Urz. UE L 168 z 30.06.2017, str. 12); Niniejszy materiał nie stanowi także rekomendacji, zaproszenia, ani usług doradztwa. prawnego, podatkowego, finansowego lub inwestycyjnego, związanego z inwestowaniem w jakiekolwiek papiery wartościowe. Materiał ten nie może stanowić podstawy do podjęcia decyzji o dokonaniu jakiejkolwiek inwestycji w papiery wartościowe czy instrumenty finansowe. Informacje zamieszczone w materiale nie stanowią rekomendacji w rozumieniu przepisów Rozporządzenia Parlamentu Europejskiego i Rady (UE) NR 596/2014 z dnia 16 kwietnia 2014 r. w sprawie nadużyć na rynku (rozporządzenie w sprawie nadużyć na rynku) oraz uchylające dyrektywę 2003/6/ WE Parlamentu Europejskiego i Rady i dyrektywy Komisji 2003/124/WE, 2003/125/WE i 2004/72/ WE. (Dz. U UE L 173/1 z dnia 12.06.20114). NDM S.A., nie ponosi odpowiedzialności za prawdziwość, rzetelność i kompletność oraz aktualność danych i informacji zamieszczonych w niniejszej prezentacji. NDM S.A. nie ponosi również jakiejkolwiek odpowiedzialności za szkody wynikające z wykorzystania niniejszego materiału, informacji i danych w nim zawartych. Zawartość materiału została przygotowana na podstawie opracowań sporządzonych zgodnie z najlepszą wiedzą NDM S.A. oraz przy wykorzystaniu informacji i danych publicznie dostępnych, chyba, że wyraźnie wskazano inne źródło pochodzenia danych.