Autor: Jarosław Jamka

My key takeaways:

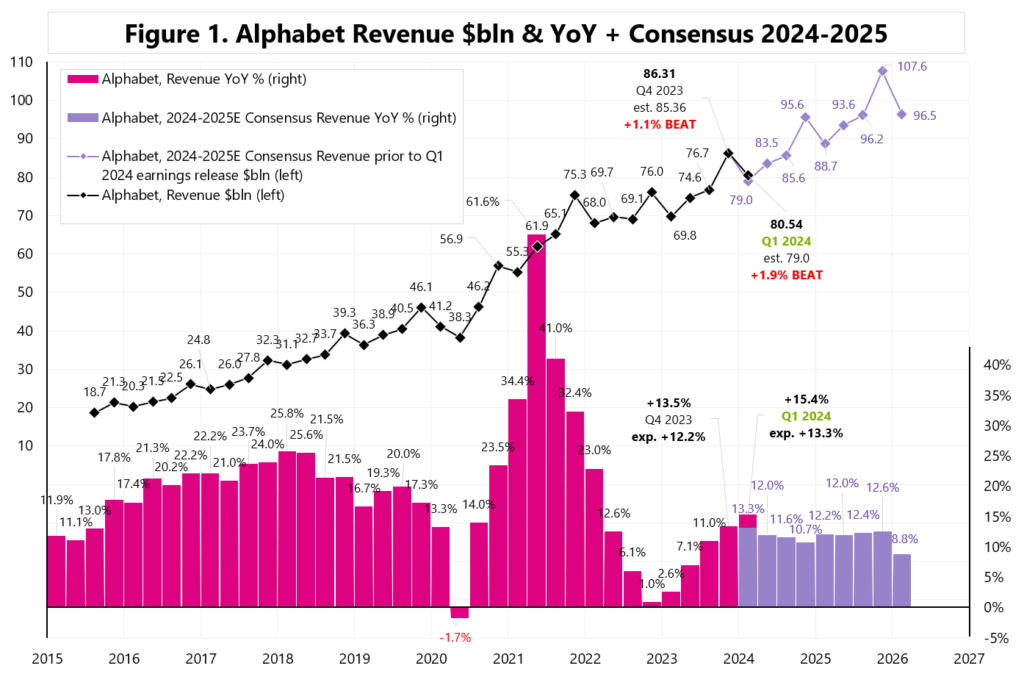

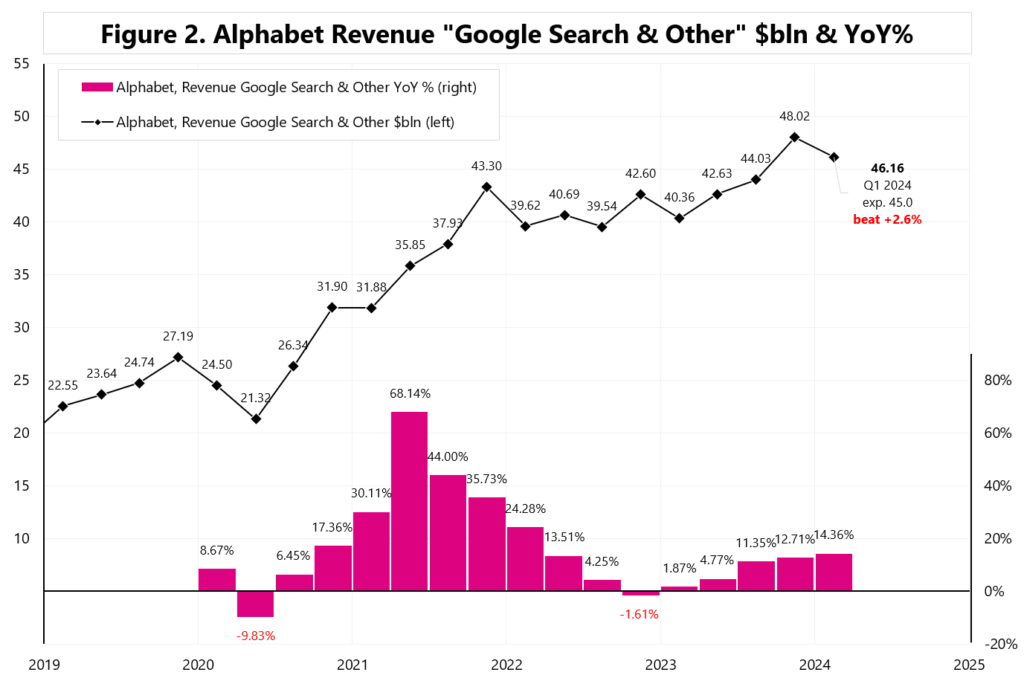

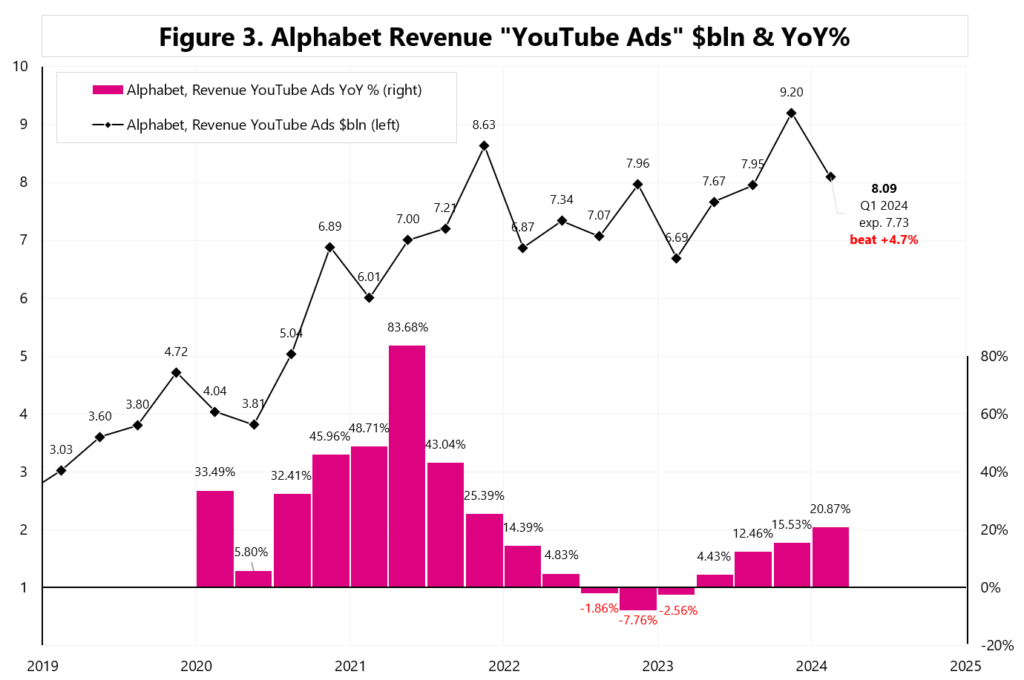

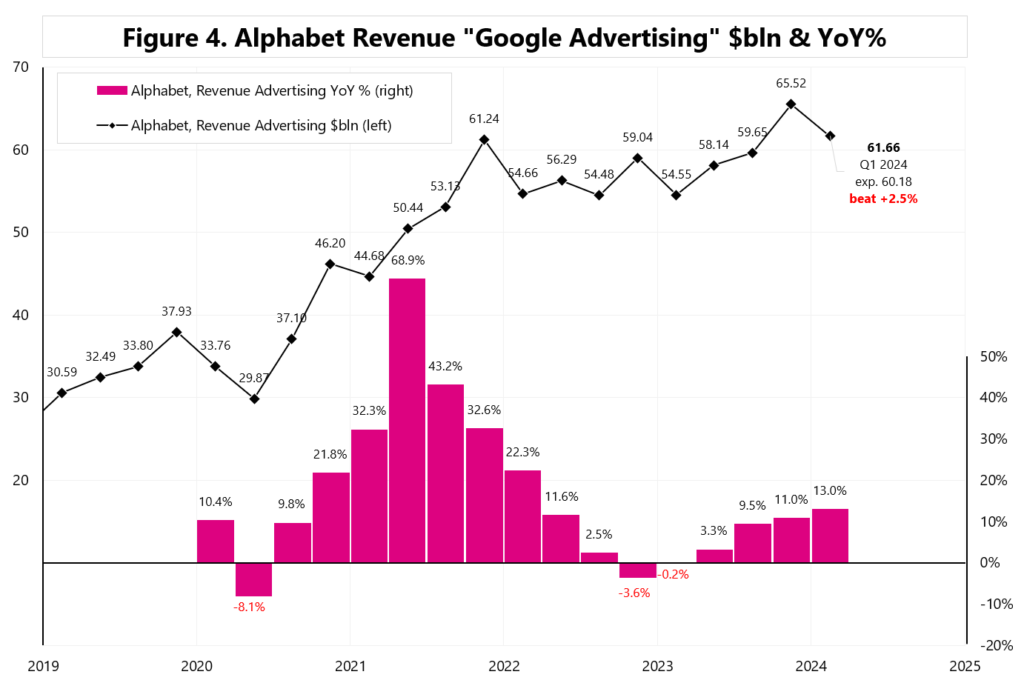

1) Alphabet rose by more than 10% after the results announcement to a new all-time high. The results were very good and practically beat expectations across the board:

+1.9% beat – Total Revenues of $80.54 billion (expected $79.0 billion), Figure 1,

+2.6% beat – „Google Search & Others” revenues at the level of $46.16 billion (expected $45.0 billion), Figure 2,

+4.7% beat – „YouTube Ads” revenues of $8.09 billion (expected $7.73 billion), Figure 3,

+2.5% beat – „Google Advertising” revenues of $61.66 billion (expected $60.18 billion), Figure 4,

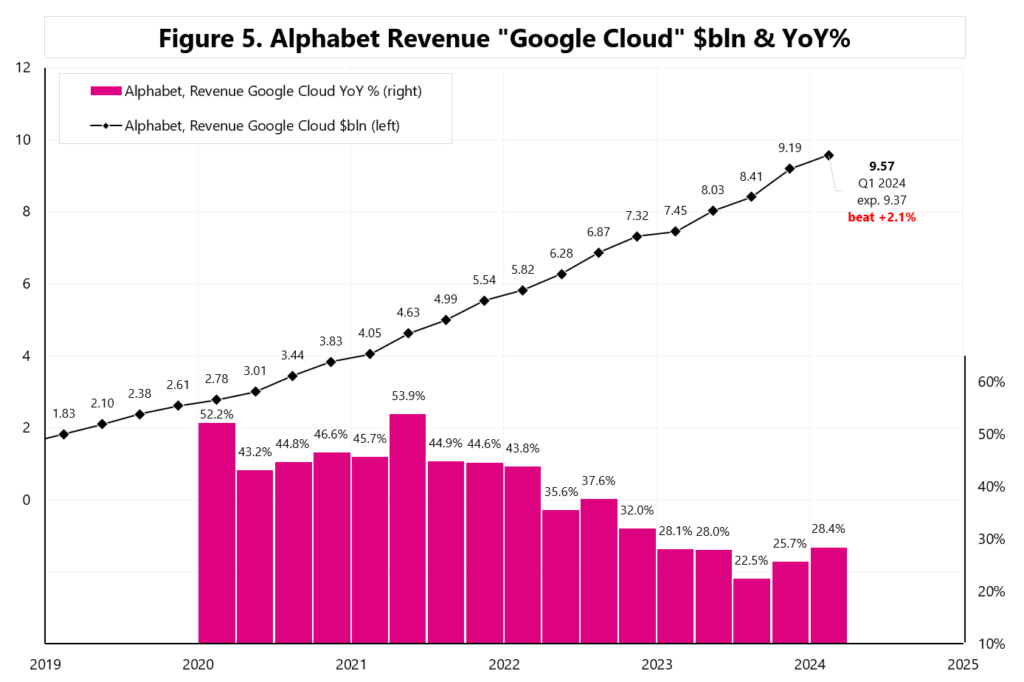

+2.1% beat – „Google Cloud” revenues of $9.57 billion (expected $9.37 billion), Figure 5,

2) The main threat to Aplhabet is a possible change in users’ preferences in using search engines and replacing them with popular AI chatbots that answer questions rather than provide links to other websites. Today, this threat is not visible in numbers, but the success of integrating the search engine with AI tools will be crucial here.

Sundar Pichai, CEO:

„AI innovations in Search are (…) perhaps the most important point I want to make. We have been through technology shifts before – to the web, to mobile and even to voice technology. Each shift expanded what people can do with Search and led to new growth. We are seeing a similar shift happening now with generative AI. (…) now, we’re starting to bring AI overviews to the main search results page. We are being measured in how we do this, focusing on areas where gen AI can improve the Search experience, while also prioritizing traffic to websites and merchants. (…) based on our testing, we are encouraged that we are seeing an increase in Search usage among people who use the new AI overviews, as well as increased user satisfaction with the results”.

On SGE (search generative experience) and Search:

“ (…) we are seeing early confirmation of our thesis that this will expand the universe of queries where we are able to really provide people with a mix of factual answers, linked to sources across the web and bring a variety of perspectives, all in an innovative way. And we have been rolling out AI overviews in the U.S. and U.K., trying to mainly tackle queries, which are more complex where we think SGE will clearly improve the experience.”

3) Alphabet showed good results in the Cloud segment, where YoY growth accelerated to 28% (+$2.12 billion YoY). Google Cloud generates revenues primarily from consumption-based fees and subscriptions received for Google Cloud Platform services, Google Workspace communication and collaboration tools, and other enterprise services.

4) Alphabet also showed a large CAPEX (purchases of property and equipment) in Q1 in the amount of $12.12 billion (expected $10.2 billion), but this did not disturb investors (in the case of Meta, the large CAPEX was cited as a negative factor). Additionally, full-year run-rate CAPEX will be at least at the Q1 level or higher, i.e. >$48 billion in 2024 (expected $43.1 billion).

5) To maintain good investor sentiment, Alphabet also announced the initiation of a cash dividend program, and declared a cash dividend of $0.20 per share that will be paid on June 17, 2024. The company intends to pay quarterly cash dividends in the future, subject to review and approval by the company’s Board of Directors in its sole discretion. Additionally, Alphabet’s Board of Directors authorized the company to repurchase up to an additional $70.0 billion of its Class A and Class C shares.

Niniejszy materiał jest informacją reklamową. Ma charakter edukacyjno-informacyjny i stanowi wyraz własnych ocen, przemyśleń i opinii autora. Niniejszy materiał służy jedynie celom informacyjnym i nie stanowi oferty, w tym oferty w rozumieniu art. 66 oraz zaproszenia do zawarcia umowy w rozumieniu art. 71 ustawy z dnia 23 kwietnia 1964 r. – Kodeks cywilny (t.j. Dz. U. z 2020 r. poz. 1740, 2320), ani oferty publicznej w rozumieniu art. 3 ustawy z dnia 29 lipca 2005 r. o ofercie publicznej i warunkach wprowadzania instrumentów finansowych do zorganizowanego systemu obrotu oraz o spółkach publicznych (t.j. Dz. U. z 2022 r. poz. 2554, z 2023 r. poz. 825, 1723) czy też oferty publicznej w rozumieniu art 2 lit d) Rozporządzenia Parlamentu Europejskiego i Rady (UE) 2017/1129 z dnia 14 czerwca 2017 r. w sprawie prospektu, który ma być publikowany w związku z ofertą publiczną papierów wartościowych lub dopuszczeniem ich do obrotu na rynku regulowanym oraz uchylenia dyrektywy 2003/71/WE (Dz. Urz. UE L 168 z 30.06.2017, str. 12); Niniejszy materiał nie stanowi także rekomendacji, zaproszenia, ani usług doradztwa. prawnego, podatkowego, finansowego lub inwestycyjnego, związanego z inwestowaniem w jakiekolwiek papiery wartościowe. Materiał ten nie może stanowić podstawy do podjęcia decyzji o dokonaniu jakiejkolwiek inwestycji w papiery wartościowe czy instrumenty finansowe. Informacje zamieszczone w materiale nie stanowią rekomendacji w rozumieniu przepisów Rozporządzenia Parlamentu Europejskiego i Rady (UE) NR 596/2014 z dnia 16 kwietnia 2014 r. w sprawie nadużyć na rynku (rozporządzenie w sprawie nadużyć na rynku) oraz uchylające dyrektywę 2003/6/ WE Parlamentu Europejskiego i Rady i dyrektywy Komisji 2003/124/WE, 2003/125/WE i 2004/72/ WE. (Dz. U UE L 173/1 z dnia 12.06.20114). NDM S.A., nie ponosi odpowiedzialności za prawdziwość, rzetelność i kompletność oraz aktualność danych i informacji zamieszczonych w niniejszej prezentacji. NDM S.A. nie ponosi również jakiejkolwiek odpowiedzialności za szkody wynikające z wykorzystania niniejszego materiału, informacji i danych w nim zawartych. Zawartość materiału została przygotowana na podstawie opracowań sporządzonych zgodnie z najlepszą wiedzą NDM S.A. oraz przy wykorzystaniu informacji i danych publicznie dostępnych, chyba, że wyraźnie wskazano inne źródło pochodzenia danych.