Autor: Jarosław Jamka

My key takeaways:

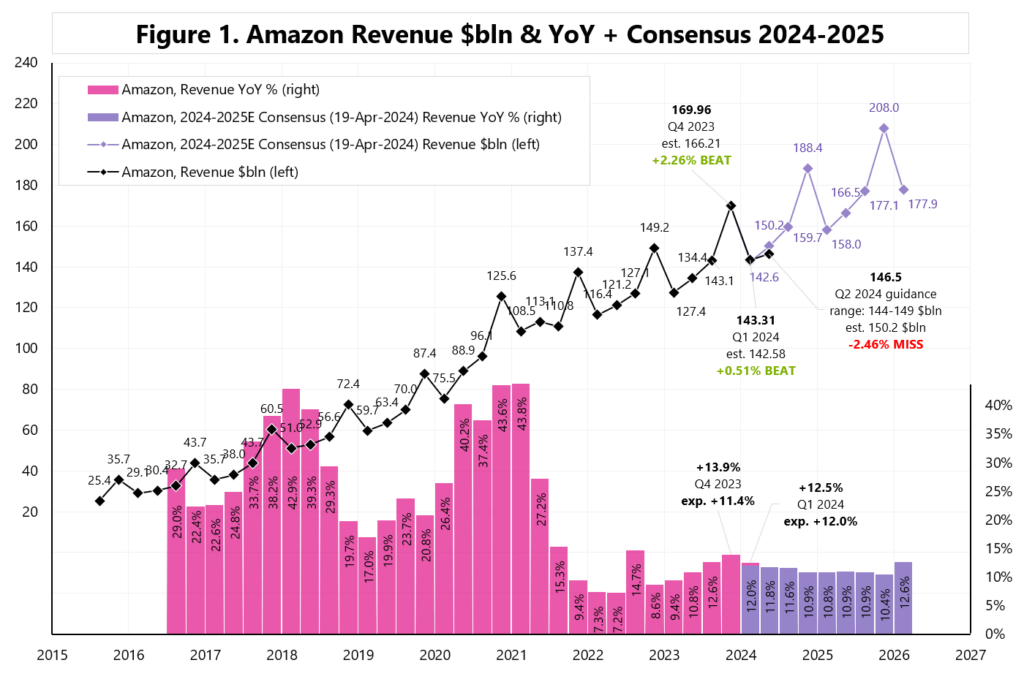

1) Total revenues increased by 12.5% YoY (above expectations, but only +0.51% beat), but at the same time the company’s guidance for Q2 disappointed … mid-range is only $146.5 billion, which means a 2.46% miss – see Figure 1.

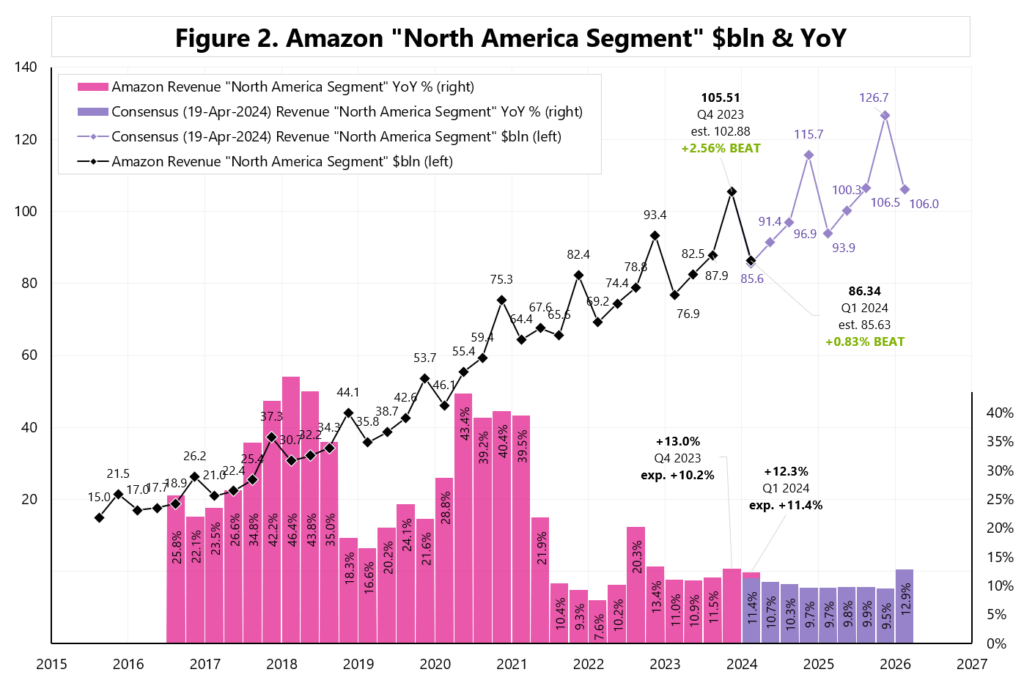

The „North America” segment performed slightly better +0.83% beat – see Figure 2.

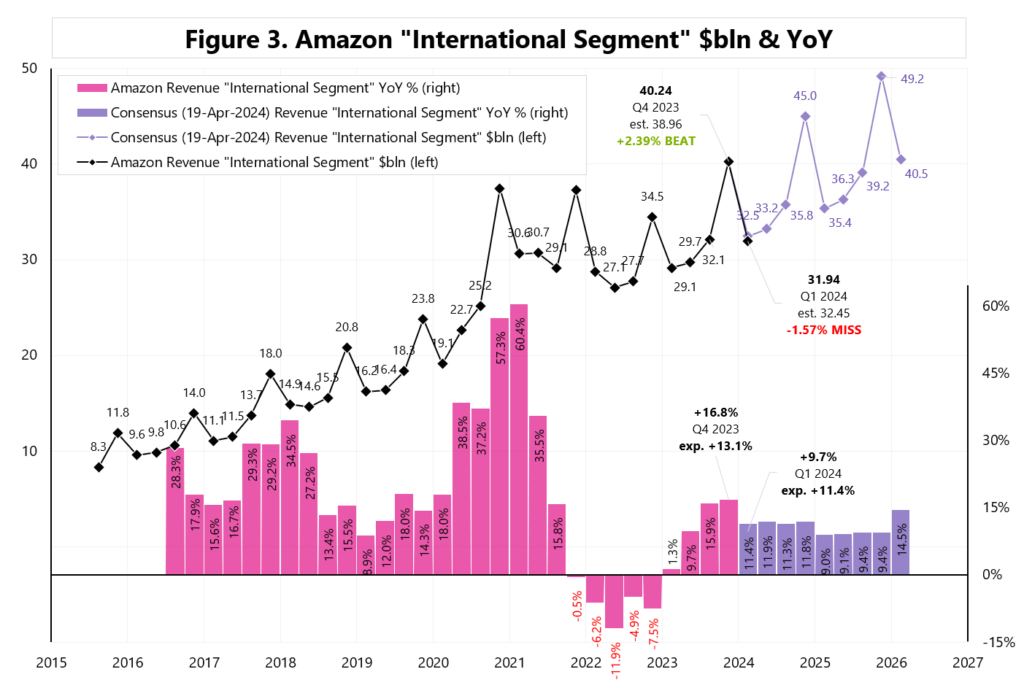

However, the „International” segment was disappointing – 1.57% miss – Figure 3.

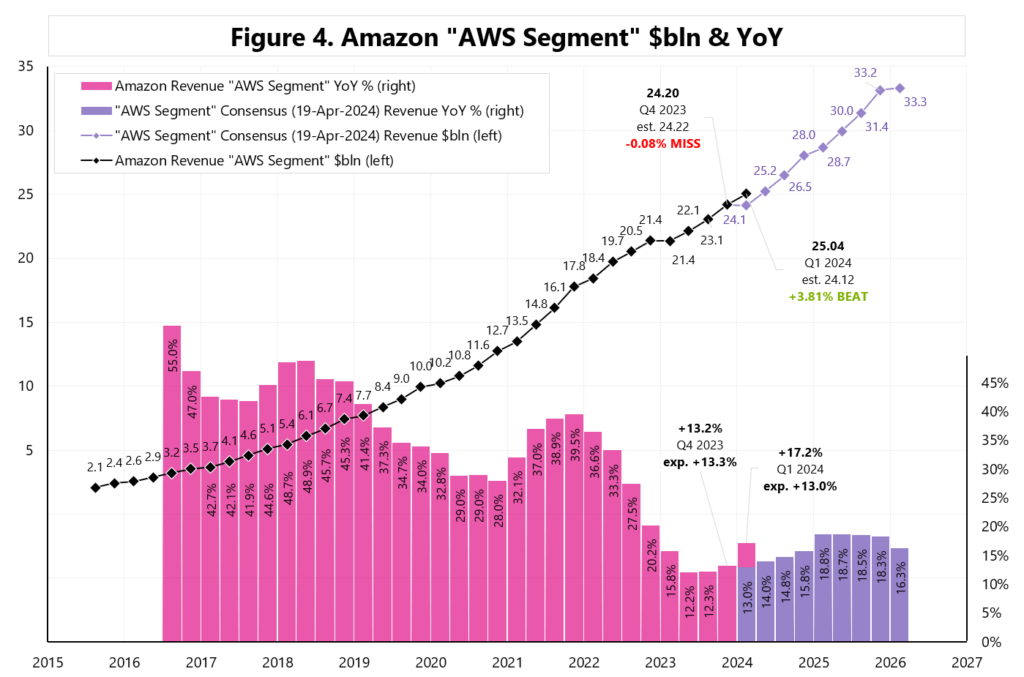

2) But the most important segment for investors, AWS (amazon web services), was the strongest! Beating expectations by as much as 3.81% – see Figure 4.

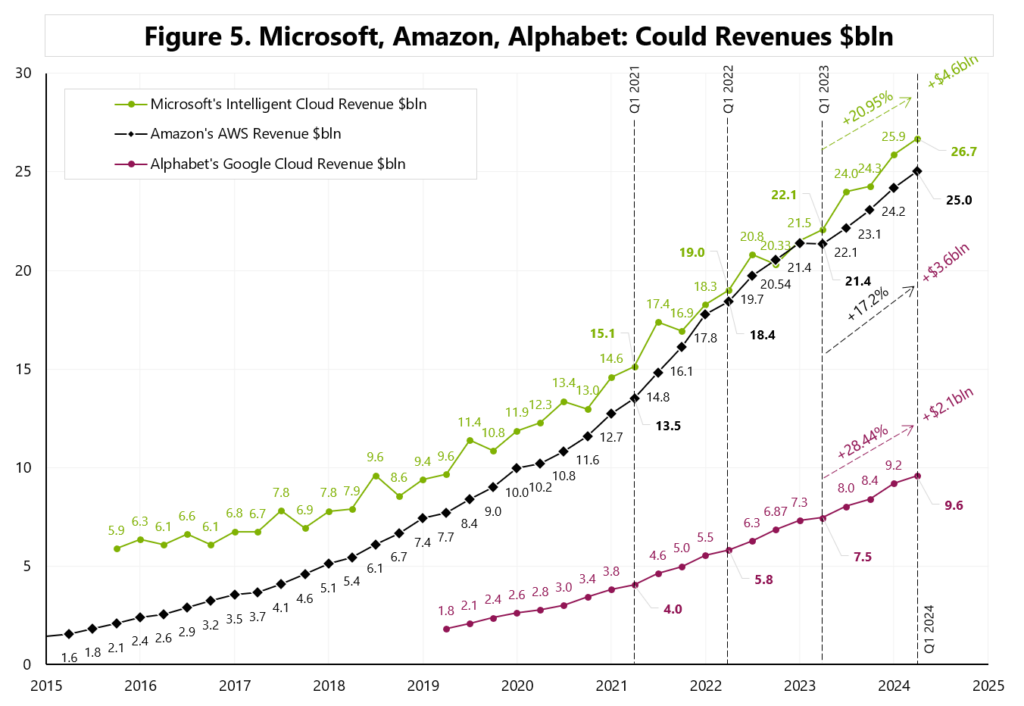

YoY growth accelerated to 17.2% (from 13.2% in Q4 2023). Figure 5 shows a comparison of the cloud businesses of Microsoft and Google.

About AWS, Andy Jassy, CEO:

“We remain very bullish on AWS. We’re at $100 billion-plus annualized revenue run rate, yet 85% or more of the global IT spend remains on-premises. And this is before you even calculate GenAI, most of which will be created over the next 10 to 20 years from scratch and on the cloud.”

„We’re seeing a few trends right now. First, companies have largely completed the lion’s share of their cost optimization and turned their attention to newer initiatives (…) Our AWS customers are also quite excited about leveraging GenAI to change the customer experiences and businesses. We see considerable momentum on the AI front”

About 3 layers of GenAI:

“(…) we continue to add capabilities at all three layers of the GenAI stack.

At the bottom layer, which is for developers and companies building models themselves, we see excitement about our offerings. We have the broadest selection of NVIDIA compute instances around, but demand for our custom silicon, training, and inference is quite high, given its favorable price performance benefits relative to available alternatives (…)

The middle layer of the stack is for developers and companies who prefer not to build models from scratch, but rather seek to leverage an existing large language model, or LLM, customize it with their own data, and have the easiest and best features available to deploy secure high-quality, low-latency, cost-effective production GenAI apps. This is why we built Amazon Bedrock (…) Bedrock already has tens of thousands of customers, including Adidas, New York Stock Exchange, Pfizer, Ryanair, and Toyota. In the last few months, Bedrock’s added Anthropic’s Claude 3 models, the best-performing models in the planet right now; Meta’s Llama 3 models; Mistral’s Various models, Cohere’s newest models, and new first-party Amazon Titan models. (…)

The top of the stack are the GenAI applications being built. And today, we announced the general availability of Amazon Q, the most capable generative AI-powered assistant for software development and leveraging company’s internal data. On the software development side, Q doesn’t just generate code, it also tests code, debugs coding conflicts, and transforms code from one form to another. Today, developers can save months using Q to move from older versions of Java to newer, more secure and capable ones.”

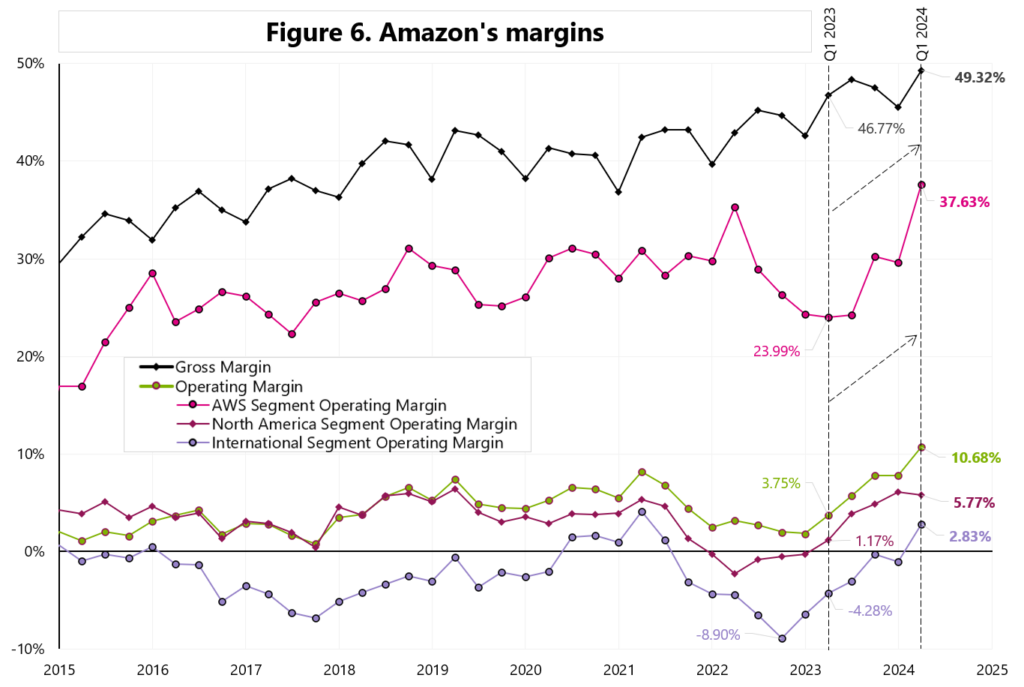

3) Margins are up significantly! Gross margin and operating margin are the highest in recent years. AWS margins have also increased to historic levels. See Figure 6.

4) Capex is up significantly! Of course, just like in Tesla, Alphabeth, Microsoft, Meta – it’s mainly AI related!

CEO:

„We expect the combination of AWS’ reaccelerating growth and high demand for GenAI to meaningfully increase year-over-year capital expenditures in 2024, which given the way the AWS business model works is a positive sign of the future growth. The more demand AWS has, the more we have to procure new data centers, power and hardware. And as a reminder, we spend most of the capital upfront. But as you’ve seen over the last several years, we make that up in operating margin and free cash flow down the road as demand steadies out. And we don’t spend the capital without very clear signals that we can monetize it this way.”

Brian Olsavsky, CFO:

“As a reminder, we define these as the combination of capex plus equipment finance leases. In 2023, overall capital investments were $48.4 billion. As I mentioned, we’re seeing strong AWS demand in both generative AI and our non-generative AI workloads, with customers signing up for longer deals, making bigger commitments. (…) We anticipate our overall capital expenditures to meaningfully increase year over year in 2024, primarily driven by higher infrastructure capex to support growth in AWS, including generative AI.”

Niniejszy materiał jest informacją reklamową. Ma charakter edukacyjno-informacyjny i stanowi wyraz własnych ocen, przemyśleń i opinii autora. Niniejszy materiał służy jedynie celom informacyjnym i nie stanowi oferty, w tym oferty w rozumieniu art. 66 oraz zaproszenia do zawarcia umowy w rozumieniu art. 71 ustawy z dnia 23 kwietnia 1964 r. – Kodeks cywilny (t.j. Dz. U. z 2020 r. poz. 1740, 2320), ani oferty publicznej w rozumieniu art. 3 ustawy z dnia 29 lipca 2005 r. o ofercie publicznej i warunkach wprowadzania instrumentów finansowych do zorganizowanego systemu obrotu oraz o spółkach publicznych (t.j. Dz. U. z 2022 r. poz. 2554, z 2023 r. poz. 825, 1723) czy też oferty publicznej w rozumieniu art 2 lit d) Rozporządzenia Parlamentu Europejskiego i Rady (UE) 2017/1129 z dnia 14 czerwca 2017 r. w sprawie prospektu, który ma być publikowany w związku z ofertą publiczną papierów wartościowych lub dopuszczeniem ich do obrotu na rynku regulowanym oraz uchylenia dyrektywy 2003/71/WE (Dz. Urz. UE L 168 z 30.06.2017, str. 12); Niniejszy materiał nie stanowi także rekomendacji, zaproszenia, ani usług doradztwa. prawnego, podatkowego, finansowego lub inwestycyjnego, związanego z inwestowaniem w jakiekolwiek papiery wartościowe. Materiał ten nie może stanowić podstawy do podjęcia decyzji o dokonaniu jakiejkolwiek inwestycji w papiery wartościowe czy instrumenty finansowe. Informacje zamieszczone w materiale nie stanowią rekomendacji w rozumieniu przepisów Rozporządzenia Parlamentu Europejskiego i Rady (UE) NR 596/2014 z dnia 16 kwietnia 2014 r. w sprawie nadużyć na rynku (rozporządzenie w sprawie nadużyć na rynku) oraz uchylające dyrektywę 2003/6/ WE Parlamentu Europejskiego i Rady i dyrektywy Komisji 2003/124/WE, 2003/125/WE i 2004/72/ WE. (Dz. U UE L 173/1 z dnia 12.06.20114). NDM S.A., nie ponosi odpowiedzialności za prawdziwość, rzetelność i kompletność oraz aktualność danych i informacji zamieszczonych w niniejszej prezentacji. NDM S.A. nie ponosi również jakiejkolwiek odpowiedzialności za szkody wynikające z wykorzystania niniejszego materiału, informacji i danych w nim zawartych. Zawartość materiału została przygotowana na podstawie opracowań sporządzonych zgodnie z najlepszą wiedzą NDM S.A. oraz przy wykorzystaniu informacji i danych publicznie dostępnych, chyba, że wyraźnie wskazano inne źródło pochodzenia danych.